One key benefit of USTC staking is that it rewards on-chain users over idle CEX liquidity, bringing USTC back where it matters: On-chain. On-chain participants deserve to be incentivized.

3 Likes

Thanks for the reply. The clarifications don’t address the core concerns.

On Proof of Stake networks, emissions pay for security. That is an example of minting serving a productive function. In ATOM’s case specifically, market cap has underperformed the wider crypto market over the last year, and price has declined even more sharply. Emissions, while necessary for security, have still been a net economic drag. By contrast the 2021–22 bullish market conditions allowed inflationary rewards to contribute to blow-off tops. The broader market today is not one where emissions, whether sourced from the Community Pool or from minting, will create positive reflexivity.

More broadly, once a proposal like this is publicly introduced, the market will begin pricing in the possibility of treasury release and future dilution. Because rational investors discount future outcomes into present prices, even a relatively small chance of this framework passing should have reduced USTC’s target valuation relative to where it otherwise would have been.

The other points from my previous post also remain unanswered:

- The framework lacks a sustainable yield source beyond CP release first and dilution later. Whether or not minting starts at launch is irrelevant, the economic dangers are similar.

- Paying yield from treasury assets without external cash flows is still subsidy, not value creation. Gradual CP distribution does not make that yield sustainable.

- The market conditions needed to drive USTC growth via reducing circulating supply simply do not exist today. That dynamic did help in prior bull-market conditions, but those market conditions simply do not exist today.

- APR funded by non productive USTC, whether from CP release or from minting creates two reflexive risks: stakers sell yield into strength, and repeg-focused holders exit because the recovery thesis is weakened.

- On-chain activity is only valuable when it is productive, not when it is a holder subsidy.

- If the goal is to increase on-chain activity, a better approach would be to ring-fence any CP USTC released and use it only for productive purposes such as lending, liquidity, or collateral, with protections to preserve or grow CP USTC holdings over time.

My core objection remains the same. Staking by itself does not create value, and without external cash flows this is still a subsidy framework rather than a sustainable recovery model.

1 Like

Thank you again for the feedback.

I think the main disagreement here is in the assumptions.

This model does not rely on immediate minting , emissions are set to 0 and only considered later based on real data and a separate governance vote. So the “reflexive dilution” scenario you describe is not present.

On sell pressure:

- Rewards are distributed gradually, not released at once

- At the same time, the system targets locking a significant portion of supply (~2B USTC)

→ This shifts supply from liquid → non-liquid, which structurally reduces sell pressure

On value:

You’re correct that staking alone doesn’t create value , but the objective here is to move activity on-chain, where value can be generated (fees, usage, integrations like MM2, etc.).

Regarding your suggestion (lending/liquidity/collateral), those are valid paths , but they also require on-chain USTC liquidity and participation first, which this proposal helps establish.

Appreciate the discussion ![]()

Thanks. We’re talking past each other, so let me be as clear as possible about our disagreement.

The issue is source of yield, not timing of minting.

My objection is not about immediate minting. My objection is to funding APR with non-productive USTC, whether that USTC comes from Community Pool release first or from minting later.

So saying “minting is 0 at launch” does not address the issue. In fact, it highlights it. CP-funded APR without external cash flows is still subsidy, not value creation, and that is exactly why minting later is even being discussed.

If Community Pool USTC were allocated to real on-chain activity rather than holder subsidies, CP USTC holdings would remain stable or even grow over time instead of shrinking.

That is also why simply reducing circulating supply by locking USTC into staking does not solve the problem. If yield were funded by real external cash flows, then USTC sold by stakers would be offset by purchases generated by those cash flows. In this proposal, there is no such offset.

Productive use of USTC to support real on-chain economic activity creates positive reflexivity: external cash flows generate USTC demand, and that demand can fund yields while offsetting stakers who sell.

Non-productive use of USTC to fund a holder subsidy creates the opposite dynamic: a race to the bottom, where actors are incentivized to exit first, especially because even modest selling pressure can have outsized price impact under current low-liquidity conditions.

So from my perspective, the clarifications to your framework still do the same thing: it drains the Community Pool first, then leaves minting on the table for later. That is a subsidy model, not a recovery model.

2 Likes

Since you want people to give feedback on here, I’ll post exactly what I posted on my X profile so no audiences miss out the discussion:)

![]()

![]()

![]()

I’ve read through this in full, and while the idea of increasing USTC utility through staking sounds positive on the surface, there’s a major concern here that can’t be ignored.

Staking fundamentally requires a continuous reward source. That’s not optional - it’s the core of how staking systems function. The proposal lists several potential funding routes (community pool, external funding, protocol revenue), but also includes minting as a long-term option.

![]() This is where the problem starts.

This is where the problem starts.

Right now, minting is framed as something that may or may not happen. But once staking is live and people begin locking their USTC for yield, the dynamic changes completely. You’re no longer designing a system - you’re maintaining one that users are financially dependent on.

If rewards begin to fall short - whether that’s due to depletion of the community pool, inconsistent external funding, or insufficient protocol revenue - the pressure to maintain those rewards doesn’t disappear. It increases.

At that point, the conversation shifts from: “Should we mint?” to: “How do we sustain rewards without minting?”

And if no sufficient real yield exists, the answer becomes obvious.

![]() That’s the concern here - not that minting is explicitly required today, but that this structure naturally leads to minting becoming the path of least resistance later.

That’s the concern here - not that minting is explicitly required today, but that this structure naturally leads to minting becoming the path of least resistance later.

Once users are staking, reducing or removing rewards isn’t a neutral decision:

-It discourages participation

-It unlocks supply back into the market

-It creates immediate negative sentiment

![]() So governance becomes incentivized to maintain rewards at all costs. And the easiest, most scalable way to do that is minting.

So governance becomes incentivized to maintain rewards at all costs. And the easiest, most scalable way to do that is minting.

That’s not speculation - it’s how these systems behave.

USTC has already suffered from mechanisms that relied on creating supply without underlying value. Reintroducing a system where rewards are not clearly backed by sustainable, real yield risks repeating the same pattern in a different form.

If staking is to be considered, then the key question needs answering upfront:

![]() Where do the rewards come from long-term - without minting?

Where do the rewards come from long-term - without minting?

Not assumptions, not future possibilities - but clearly defined, sustainable sources.

Because if that answer isn’t solid today, then this doesn’t remove the risk of minting…

It just delays it.

![]() If minting is completely removed and not mentioned anywhere in the proposal going on governance, and you rely on actual onchain yields,MM2, ETC, for rewards (how it should be) then ill be a YES.

If minting is completely removed and not mentioned anywhere in the proposal going on governance, and you rely on actual onchain yields,MM2, ETC, for rewards (how it should be) then ill be a YES.

If there’s a slight chance of minting, or a mention of it anywhere then I will be a NO.

2 Likes

Thank you for the detailed feedback , and I appreciate you bringing it here. I would just ask that these discussions continue on the forum, as this is where the community tracks and evaluates proposals collectively.

I agree with your core point: staking requires a sustainable reward source. That’s exactly why multiple options are outlined : including fees (MM2), protocol revenue, unused/dead allocations, and only as a last option, minting.

A few important clarifications:

- Minting is NOT active at launch - it is set to 0, and only considered later through governance if needed

- Before any such decision, we will have real data after ~3 months (participation, behaviour, on-chain activity)

- By then, additional sources like MM2 and other ecosystem products are expected to contribute to rewards

So this is not “minting by design” , it is optional, controlled, and community-decided.

Also, governance is key here:

If at any point the community does not support minting, it simply does not pass.

Regarding your concern about repeating past mistakes:

The previous issue was not USTC itself, but the mechanism around it. In fact, USTC supply today (~6B) is significantly lower than pre-depeg (pick ~18B). This framework is not the same system, and is being built with safeguards and staged rollout.

Finally, on your point:

“Where do rewards come from long-term without minting?”

That is exactly why we start with:

- Community Pool (gradual distribution)

- On-chain growth → fees

- New products (MM2, etc.)

And only later evaluate if anything else is needed.

If those sources are sufficient, minting is never required.

Appreciate your support for USTC staking overall, and for raising these concerns ![]()

USTC Staking System - Signal Proposal (Community Direction)

Summary

This proposal is a signal proposal to determine if the community supports initiating work on the creation of a native USTC staking system on Layer 1.

It does not implement any technical changes, allocate funds, or introduce minting.

It only asks whether the community wants development to begin.

Main Goal

The goal of this proposal is to ask:

Should development work begin on a USTC staking system aimed at expanding utility and supporting long-term recovery efforts?

A “Yes” vote signals that the community supports moving forward to the next stage of development.

Scope of This Proposal

This proposal is non-binding and limited to:

- Signaling community interest

- Providing direction to developers

- Establishing the first step of a phased approach

No minting

No Community Pool usage

No parameter changes

No implementation at this stage

Proposed Phased Approach

If this signal proposal passes, the process will follow a structured path:

Phase 1 - Technical Development Proposal

A separate technical proposal will be submitted by developers to:

- Create the USTC staking system infrastructure

- Implement required modules (oracle pool, distribution logic, parameters, etc.)

At this stage:

- No minting

- No Community Pool funds used

Phase 2 - Funding & Activation

Only after the system is built and ready:

- A proposal for Community Pool allocation (to fund rewards)

- Followed by a proposal to activate rewards parameters

Phase 3 - Review & Future Decisions

After launch:

- A review period to analyse staking participation and system performance

- Future decisions (including any emissions or additional funding mechanisms) will be:

- Data-driven

- Governance-controlled

- Optional

Why This Approach

This staged approach ensures:

- Full community control at every step

- No upfront risk (no funds or minting involved)

- Ability to evaluate progress before committing further

Voting Options

- Yes → Support starting development work on a USTC staking system

- No → Do not proceed with development

Conclusion

This is the first step to evaluate whether the community wants to explore a structured path toward USTC utility expansion through staking.

A Yes vote does not implement the system , it only allows work to begin.

1 Like

Im sorry but that’s a generic reply you keep giving everyone.

As you’ve again stated that minting is an option going forward, then I’ll be a NO on the proposal.

Until the minting part is rectified and will never be an option, or a relied on backup plan, then i’ll stay a NO.

This needs a serious rethink and overhaul, to rely on chain yields for staking rewards .

P.s. I’ll vote YES to a signalling proposal to start creating a USTC staking plan, on one condition the development proposal does NOT include minting ANYWHERE, not even a thought about minting on the future ![]()

2 Likes

Validator Position on USTC Staking Signal Proposal

We appreciate the intent behind this signal proposal and support exploring new avenues to expand USTC utility and contribute to long-term ecosystem recovery.

As a validator, we are open to supporting the development of a USTC staking system provided it adheres to a set of clear economic and structural principles that ensure sustainability, real value creation, and alignment with the broader ecosystem.

Core Principles for Support

1. Real Yield Generation

The system must generate actual revenue from productive on-chain activity (e.g. lending, liquidity provisioning, structured strategies), rather than relying on purely redistributive or artificial incentives.

2. No Meaningful Supply Dilution

There should be no dilution of circulating USTC supply, except potentially minimal emissions as a carefully controlled incentive mechanism. Ideally the current dilution via regular LUNC staking can be minimized by introducing the USTC staking system.

3. Community Pool Integrity

Any use of Community Pool funds must ensure that:

- Ownership remains with the Community Pool at all times

- Funds may be deployed into productive positions (e.g. vaults, LPs, lending markets)

- Capital is not spent, but strategically allocated to generate yield

4. No USTC or LUNC Minting

Under no circumstances should this system rely on minting new USTC or LUNC.

5. Productive Use of Oracle/Distribution Flows (Bonus)

A strong advantage would be a design that redirects existing oracle or distribution flows toward productive use cases that benefit the chain, rather than using them for artificial staking rewards or validator commission structures.

Our Preferred Direction

Rather than a traditional staking model that redistributes existing capital, we encourage a more productive and capital-efficient approach:

An intelligent USTC vault system that:

- Accepts USTC deposits (including vesting positions)

- Actively deploys capital across multiple on-chain venues

- Generates yield through real strategies such as:

- Lending (e.g. via Juris Protocol)

- Liquidity provisioning (e.g. Terraport & Garuda DEXs)

- Cross-chain opportunities (future)

- Automated / AI-assisted strategy allocation (future)

This approach ensures:

- Value is created, not merely redistributed

- USTC utility is expanded in a meaningful way

- The system contributes to organic demand and sustainability

Collaboration

We believe this can be a strong direction for the ecosystem and are open to collaboration.

Juris Protocol has expressed willingness to support and consult on the design and implementation of such systems if needed (free of charge), particularly around lending integrations and yield strategies, as well as general design concept.

Further details should be developed collaboratively with the community and relevant teams during the technical proposal phase.

Final Position

We view this signal proposal as a reasonable first step.

Our support for future phases will depend on whether the implementation:

- Aligns with the principles outlined above

- Prioritizes sustainable value creation

- Avoids short-term, extractive incentive structures

If these conditions are met, we would be inclined to support progressing to the next stages.

PS

Juris Protocol would support and vote in favor of any solution that meets the above criteria, regardless of implementation approach or participating teams.

Collaboration with Juris is optional — we do not seek to impose involvement or dictate the design, but simply offer support where useful.

4 Likes

While the proposal is well-structured, we believe it introduces inflation without creating genuine demand or redistribution mechanisms.

Staking rewards are funded by the creation of new tokens, leading to long-term dilution and continuous selling pressure.

Currently, USTC suffers not from a lack of yield, but from a lack of utility and demand.

This approach may reduce supply in the short term, but it risks undermining long-term price stability and the credibility of the ecosystem.

Market mechanisms such as MM2.0 should be prioritized over artificial yield systems.

For these reasons, Uncode Lounge validator votes NO.

1 Like

This signal proposal for a native USTC staking system on Terra Classic Layer 1 is explicitly designed as a flexible, community-driven first step. It does not rely on minting new USTC or LUNC, does not mandate artificial redistribution, and directly targets meaningful supply reduction, facts that already align with or exceed every core principle listed. Here is a point-by-point factual answer to Juris requests based on the proposal text itself and current Terra Classic mechanics (as of the proposal dated March 2026).

- Real Yield Generation Is Explicitly Prioritized, Not Pure Redistribution.

The proposal states that rewards will come from protocol revenue sources (Market Module 2 arbitrage fees, DEX swap fees, gas fee allocations, burn tax redirections) and ecosystem contributions from projects. These are productive on-chain activities, exactly as the validator demands.

The Community Pool bootstrap (61 million existing USTC) is only an initial seed; long-term sustainability shifts to real revenue streams once MM2 deploys post-SDK53. This is not “purely redistributive.” The validator’s own preferred “intelligent USTC vault” (lending via Juris, LP on Terraport/Garuda) is one possible implementation of those revenue streams, but the native staking signal proposal does not preclude integrating those exact mechanisms. It simply starts with the proven Cosmos SDK staking module already used for LUNC.

- No Meaningful Supply Dilution. The Proposal Reduces Liquid Supply.

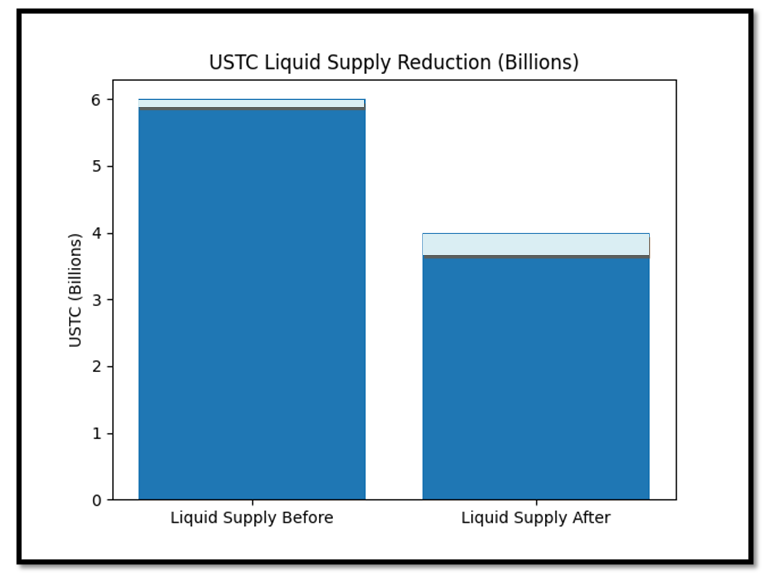

Current circulating USTC supply is approximately 5.5 billion tokens (post-2022 burns; supply never hyper-inflated like LUNC’s trillions). The proposal targets staking 20–33 % (1.2–2 billion USTC) to lock tokens on-chain, directly removing them from liquid circulation and CEX sell walls.

This is the opposite of dilution. The validator acknowledges that “the current dilution via regular LUNC staking can be minimized by introducing the USTC staking system” the proposal does exactly that by increasing overall on-chain utility and strengthening LUNC staker rewards (which already include USTC distributions). Controlled inflation is listed only as a final optional long-term funding source requiring separate governance approval, and the proposal notes USTC still sits well below its historical 18 billion peak, giving economic room if chosen. No minting is required to launch.

- Community Pool Integrity Is Preserved

The proposal suggests using a portion of the Community Pool’s existing 61 million USTC as a bootstrap reward pool. This is allocation, not spending or loss of ownership:

- Funds remain under community governance.

- They are deployed to generate staking incentives that increase on-chain activity, LUNC staking APR, and MM2 liquidity, precisely the “productive positions (e.g. vaults, LPs, lending markets)” the validator endorses.

The pool is not burned, transferred away, or removed from community control. This mirrors how the existing LUNC Oracle Pool and community-funded initiatives already operate on Terra Classic.

- No USTC or LUNC Minting Required

The proposal is crystal clear:

- Primary funding = existing CP USTC + voluntary ecosystem contributions + future protocol revenues.

- “Only native USTC… would be used for rewards.”

- Minting/inflation is not mandated and is presented solely as one possible future option after community evaluation.

This satisfies the validator’s “Under no circumstances should this system rely on minting” rule for the initial and core phases.

- Productive Use of Oracle/Distribution Flows (Already Happening + Enhanced)

LUNC delegators and validators already receive USTC as part of their reward distribution. The proposal strengthens this flow by increasing USTC demand and price through staking lockup, directly boosting the real value of those existing USTC rewards. This is the exact “redirects existing oracle or distribution flows toward productive use cases” bonus the validator highlights.

Native Staking Complements, Does Not Preclude, Vault Systems.

The validator’s “intelligent USTC vault” (deposits → lending on Juris, LP on Terraport/Garuda, etc.) is an excellent DeFi layer that can sit on top of native staking. The signal proposal is deliberately scoped to native L1 staking (simple, battle-tested Cosmos module, no smart-contract risk for core lockup) to achieve immediate supply reduction and on-chain participation. Nothing in the proposal prevents later integration of Juris-style vaults or AI strategies. Juris Protocol’s willingness to consult is noted and appreciated, but the signal proposal is implementation-agnostic and does not require any single team.

The validator concludes they “view this signal proposal as a reasonable first step” and “would be inclined to support progressing to the next stages” if the listed principles are met.

All principles are already met by the proposal text: real revenue paths, no forced minting, supply reduction via lockup, CP funds allocated (not spent), and enhancement of existing flows. The only difference is that the proposal keeps options open for the community rather than prescribing one specific vault architecture upfront.

This is a signal proposal no code changes, no immediate funding vote, no minting. It simply asks the community whether native USTC staking should be explored further. Voting it down is shutting the doors for exploration and development before Governance Approved implementation.

2 Likes